WHO IS AN EMPLOYEE?

MAINTAINING A RETIREMENT PLAN FOR YOUR EMPLOYEES IS NO EASY TASK. At various points during the year, employers and HR departments field participant questions, help with enrollments, deliver notices and statements, and participate in the distribution process. However, an additional responsibility, and one of the most important, is the collection of data that is used for compliance testing and government reporting. Though all these duties are important, one task drastically affects the outcome of your compliance testing; accurate reporting of all employee information to your third-party administrator. Sound onerous? Not really.

On the surface, this appears like an easy-to-do. Of course, you know who your employees are! But, for retirement plan purposes, do you really know who is considered an employee? The definition provided by the Employees Retirement Income Security Act (ERISA) isn’t much help. ERISA states, “The term employee means any individual employed by the employer.”. Well, that much is probably obvious. However, the answer can be much more complex than it seems and has tripped-up many well-intentioned companies. In fact, employers as large as Microsoft, Coca-Cola, and Time Warner have found themselves in litigation over this very issue.

Why does this matter? Each year, your TPA analyzes your submitted census and applies the applicable regulations to ensure that the plan is in compliance with current law. Compliance items like eligibility, allowable employee and employer contribution levels, and tax deductibility (just to name a few) are calculated each year to ensure your retirement plan remains qualified, meaning that the tax-advantaged status of the funds in the plan remain tax-deferred. While your TPA may do the complicated part, the data upon which compliance work is based comes from you, the employer.

So, what do you need to know to enroll and report the proper employees? We’ve listed some common employee status types below.

W-2 EMPLOYEES: You’ve got this part! This represents any employee for which you issue a form W-2. For calendar year plans, be sure that the number of employees and compensation amounts reported match the form W-3. No matter how many, or few, hours a W-2 employee works, be sure that the information is reported for compliance purposes.

PARTNERS AND SOLE PROPRIETORS: This should include partners that report income on a Schedule K-1 or sole proprietors that report income on a Schedule C.

INDEPENDENT CONTRACTORS: For example, Aaron, the owner of a local golf club, tells Spencer, a college student looking for summer work, that he can come on board for the summer as an independent contractor. He will work as a groundskeeper, is to report to work daily from 7:30 to 5:00, and will use the club’s equipment to perform his duties. His hourly compensation will be reported on a Form 1099, no taxes will be withheld, and he will not be eligible for benefits. Both agree to these terms in writing. Is Spencer an independent contractor or an employee?

97.1% off all plans allow catch-up contributions. Only 36% match.

Unfortunately, it’s not as simple as pointing to Aaron and Spencer’s agreement or the fact that Spencer will receive a 1099 form instead of a W-2. Under audit, the IRS would focus on whether a company has the right to control the worker. There are several factors to consider, including whether the company has the right to:

- Set the work schedule,

- Establish the work location,

- Pay by the time worked rather than by the job or on commission,

- Furnish equipment for the worker’s use, and

- Require work-related training.

Based on these criteria, it is likely that Spencer would be considered an employee for retirement plan purposes. LEASED EMPLOYEES: In a different scenario, Aaron decides to engage the services of a professional employer organization (PEO) for his golf club. The PEO will provide all payroll and HR functions and is officially “the employer”. Aaron will still manage the day to day activities of the staff. Unless some extenuating circumstances exist, the employees that have been transferred to the PEO are still considered employees of Aaron’s for retirement plan purposes.

EMPLOYEES OF A CONTROLLED GROUP OF ENTITIES: Aaron, who still owns the local golf club, decides to purchase a company that owns a local bowling alley. The golf club sponsors a retirement plan, the bowling alley does not. Depending on several factors, including the level of ownership that Aaron has in each company, the employees of the bowling company could be considered as being eligible for retirement plan benefits.

Aaron decides that he will put the company that owns the bowling alley in his daughter Annabelle’s name. Does this change the outcome? The answer is no. Due to laws that govern attribution of ownership among family members, you’ll need to report any other companies owned by shareholders, and shareholders’ family members, to your TPA.

EMPLOYEES OF AN AFFILIATED SERVICE GROUP (ASG): An ASG works similarly to a controlled group of entities regarding an employee’s eligibility for retirement benefits. Determination of the existence of an ASG is complicated, so alert your TPA if your firm is affiliated with other entities. An example of an ASG would be a service organization that provides both regular and continuing management functions for affiliated, but separate, companies.

SHARED EMPLOYEES: A shared employee is someone who works for more than one business at a time. If those businesses are “controlled or affiliated” as described above, all compensation for the shared employee could be considered for benefit purposes. For example, if Aaron asks Spencer to work at both the golf club and the bowling alley, and the

companies are considered a controlled group of entities or an ASG, all of Spencer’s hours and compensation would be included for benefit purposes.

EXCLUDED CLASSES OF EMPLOYEES: Aaron’s golf club maintains a plan for the benefit of his employees. Under the terms of the plan, groundskeepers are not eligible for benefits. Retirement plans can be designed with certain groups excluded from benefits. This does not change the importance of reporting employees like Spencer for compliance testing purposes. Benefit exclusions are still subject to coverage testing each year, making it important to accurately report all employees regardless of class (if stated in the plan document, collectively bargained employees have an unlimited exclusion). Be especially careful to report seasonal and part-time employees, as both of these groups are subject to testing.

Plan Sponsors need not become retirement plan professionals to make the determination of who is eligible for their plan’s benefits. Ask your TPA for guidance about any employee relationships that might affect your retirement plan.

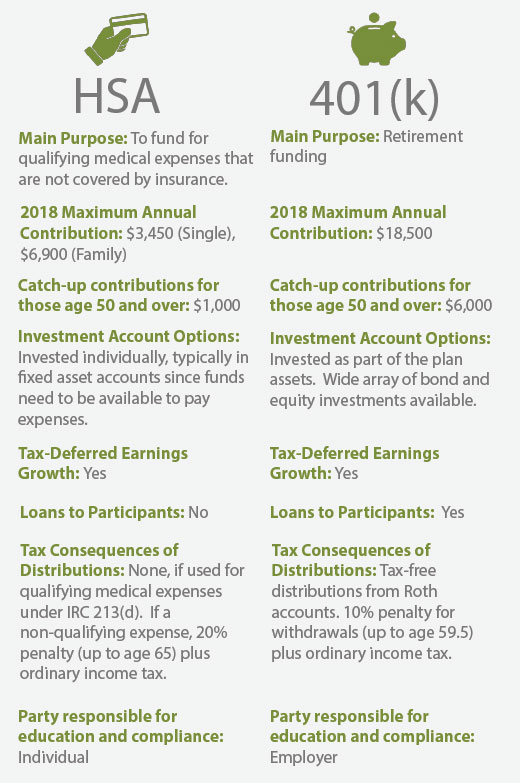

HSA vs. 401(k)

IF YOUR COMPANY HAS DECIDED TO OFFER A HIGH DEDUCTIBLE HEALTH PLAN, DON’T WORRY, YOU ARE NOT ALONE. Recent studies show that an increasing number of employers have elected to offer high deductible health plans (HDHP) either to completely replace or be offered in conjunction with a more traditional Health Maintenance Organization (HMO) plan or Preferred Provider Organization (PPO) plan. When sponsoring an HDHP, employers typically offer their employees the ability to contribute to a Health Savings Account (HSA) to help offset the increased deductible associated with the HDHP. In 2015, 24 percent of all workers were enrolled in a HDHP with an HSA savings option. This is a dramatic rise since 2009 when just 8 percent were covered under such plans.

Contributions to an HSA are tax-deferred, like those in 401(k) plans, allowing employees to pay for qualifying medical expenses with pre-tax dollars. If your firm sponsors a 401(k) plan in addition to an HSA, an employee now has two programs to which they can allocate their savings dollars. But, can HSAs have a negative effect on 401(k) savings? In a perfect world, employees would maximize both plans, as they serve different but equally important roles in an employee’s overall financial picture. Therefore, while there are many differences between HSA and 401(k) plans, by understanding a few key items participants can make informed decisions and elections to optimize both plans for their financial well-being. A few of these key items are outlined in the accompanying infographic.

Who is eligible to participate in an HSA? To be considered an eligible individual in 2018, an employee must meet the following requirements:

-

- He or she cannot be enrolled in Medicare.

- The employee cannot be claimed as a dependent on another’s 2017 tax return.

- The employee is covered under a high deductible health

plan (in 2018 a HDHP must have a minimum deductible of

$1,350 for single coverage and $2,700 for family coverage,

and a maximum deductible or out-of-pocket expense of

$6,650 for single coverage and $13,300 for family coverage). - The employee mustn’t have any other coverage that

would be considered general health insurance coverage

(coverage for specific illnesses, dental or vision coverage,

and long-term care insurance is not considered other

coverage for determining eligibility. For a full listing, see

IRS Publication 969 (www.irs.gov/publications/p969)).

Though many HSAs are funded by employer payroll deductions, an employee may fund their HSA by simply writing a check to their account. Both, employers and employees, can contribute to an HSA in the same year; however, the combined contribution amount is subject to the IRS’s annual plan contribution limits. Contributions must be made in cash. No contributions of stock or property are allowed.

Making a choice about how to invest their available savings pool is not new for employees. Helping your employees to understand the different purposes of each plan will aid with decisions that affect their financial well-being.