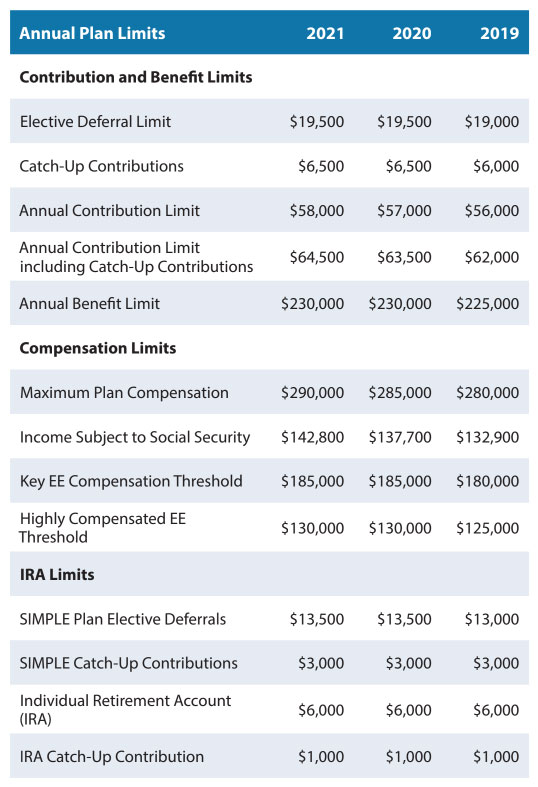

COST OF LIVING ADJUSTMENTS FOR 2021

ON OCTOBER 26, 2020, THE IRS ANNOUNCED THE COST OF LIVING ADJUSTMENTS AFFECTING THE DOLLAR LIMITATIONS FOR RETIREMENT PLANS. Contribution and benefit increases are intended to allow participant contributions and benefits to keep up with the “cost of living” from year to year. Here are the highlights from the 2021 limits:

The elective deferral limit remains unchanged at $19,500. This deferral limit applies to each participant on a calendar year basis. The limit applies to 401(k) plans, including Roth and pre-

tax contributions, 403(b), and 457(b) plans.

- Catch-up contributions remain unchanged at $6,500 and are available to all participants age 50 and older in 2021.

- The maximum dollar amount that can be contributed to a participant’s retirement account in a defined contribution plan increased from $57,000 to $58,000. The limit includes both employee and employer contributions as well as any allocated forfeitures. For those over age 50, the annual addition limit increases by $6,500 to include catch-up contributions.

- The annual benefit limit which applies to participants in a defined benefit plan remains unchanged at $230,000.

- The maximum amount of compensation that can be considered in retirement plan compliance has been raised to $290,000. In addition, income subject to Social Security taxation has

increased to $142,800. - Thresholds for determining highly compensated and key employees remain unchanged at $130,000 and $185,000, respectively.

If you have any questions on how these increases can affect your plan, please contact your representative.

CYCLE 3 PLAN DOCUMENT RESTATEMENTS

APPROXIMATELY EVERY SIX YEARS, THE IRS REQUIRES THAT PRE-APPROVED QUALIFIED RETIREMENT PLANS UPDATE (OR RESTATE) THEIR PLAN DOCUMENT TO REFLECT RECENT LEGISLATIVE AND REGULATORY CHANGES. Plan restatements are divided into staggered six-year cycles depending on the type of plan (e.g. defined benefit plans or defined contribution plans, such as 401(k) and 403(b) plans). In Announcement 2020-7, the IRS confirmed that the next restatement cycle for pre-approved defined contribution plans is a 24-month period that began August 1, 2020 and will close on July 31, 2022. This restatement cycle is known as the “Cycle 3” restatement, as it is the third required restatement under the pre-approved retirement plan program.

What is a plan restatement? A restatement is a complete re-writing of the plan document. Along with mandatory regulatory changes, the restated document incorporates all voluntary amendments adopted since the last time the document was updated.

What is a pre-approved document? A pre-approved document is one that has fixed provisions and pre-approved choices that can be selected by the plan sponsor. The fixed language and choices have been reviewed and approved by the IRS. Why is a plan restatement needed? Plan documents are drafted based on laws and regulations imposed by Congress, the IRS, and the Department of Labor (DOL). Plan documents must be updated to remain in compliance with changing laws and regulations. Since the previous restatement cycle ended on April 30, 2016, there have been several regulatory and legislative changes that impact retirement plans. To assist with the restatement process, the IRS issues a “Cumulative List of Changes,” instructing what must be included in the restated document. For this current cycle, the Cumulative List of Changes was issued in 2017. As a result, the list does not include any recent changes due to the SECURE Act or CARES Act. These changes will be addressed in separate good-faith amendments rather than in the Cycle 3 restated plan documents.

What if a plan was just established? The restatement cycle is set by the IRS without regard to a plan’s initial effective date. Since the Cycle 3 document language was just recently approved, even

newly-established plans may need to be restated.

What if a plan is terminating? The IRS requires that all documents be brought up to date with current laws and regulations before they can be terminated. As a result, your document must be amended and/or fully restated as part of the plan termination process.

What happens if a plan is not restated? Plans that do not adopt a restated plan document by the July 31, 2022 deadline will be subject to IRS-imposed penalties. Failure to timely restate the plan will also jeopardize the plan’s tax-qualified status.

Can restatement fees be paid from plan assets? Since the plan document restatement is required to maintain the plan’s tax-qualified status, the DOL allows the restatement fee to be paid from plan assets.

REQUIRED YEAR-END PARTICIPANT NOTICES

AS THE END OF THE YEAR APPROACHES, OUR TO-DO LISTS BECOME LONGER BUT OUR BANDWIDTH BECOMES CONDENSED. To compound matters, when you sponsor a retirement plan, you know you will be in close contact with your TPA firm about the various year-end notices that must be distributed to plan participants. Below is a summary of some of the most common year-end notices that may apply to calendar

year defined contribution plans:

Safe Harbor Notice – Safe harbor plans must provide an annual safe harbor notice to participants at least 30 days (but no more than 90 days) before the beginning of each plan year. The safe harbor notice informs participants of certain plan features, such as eligibility requirements, the plan’s safe harbor formula, and vesting and withdrawal provisions for plan contributions. The SECURE Act eliminated the safe harbor notice requirement for plans that only include a nonelective safe harbor contribution. If the plan also provides for a discretionary matching contribution, a safe harbor notice is still required.

Qualified Default Investment Alternatives (QDIA) Notice – If a plan utilizes a QDIA on behalf of participants or beneficiaries who fail to direct the investment of assets in their individual accounts, the plan must provide an annual QDIA notice at least 30 days (but no more than 90 days) before the beginning of each plan year. The QDIA notice provides a description of the QDIA, including its investment objectives, fees, and expenses.

Automatic Contribution Arrangement (ACA) Notice – Plans that utilize an eligible automatic contribution arrangement (EACA) or qualified automatic contribution arrangement (QACA), in the absence of an affirmative election by a participant, must provide an annual notice to participants at least 30 days (but no more than 90 days) before the beginning of each plan year. The notice includes an explanation of the ACA provisions, such as the default contribution rate, how to elect not to participate, how to change the default rate, and how to make an investment election.

Participant Fee Disclosure Notice – Participants must receive an updated annual fee disclosure notice within 14 months of the date they received their last notice. The notice includes an explanation of plan level and individual fees that may be charged against a participant’s account.

Many participant notices required by the IRS can be distributed electronically if certain conditions are met. In general, the IRS allows e-delivery if the media being used is provided by the plan sponsor and participants are required to access that media as part of the participant’s job. For additional details regarding electronic delivery of IRS notices, please contact us or see irs.gov/retirement-plans/plan-participant-employee/retirement-topics-notices.

Under new rules issued by the DOL, if a plan sponsor has complied with certain rules, including providing a Notice of Internet Availability to a participant’s electronic address, covered DOL notices can now be provided electronically as well. For additional details regarding electronic delivery of DOL notices, please contact us or see dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/fact-sheets/electronic-disclosure-safe-harbor-for-retirement-plans.

THE CARES ACT UPDATE

2020 HAS BEEN A DIFFICULT YEAR WITH MANY UNEXPECTED CHALLENGES. FOR COMPANIES THAT SPONSOR RETIREMENT PLANS, SOME OF THESE CHALLENGES CAME IN THE FORM OF THE CORONAVIRUS AID, RELIEF, AND ECONOMIC SECURITY (CARES) ACT. While the CARES Act provided much needed relief to plan sponsors and their participants, the relief also brought new complexity to retirement plan compliance.

Coronavirus-Related Distributions (CRDs) – Under the CARES Act, a qualified individual is permitted to take a distribution of up to $100,000 without being subject to the 10% penalty typically applied to distributions made prior to age 59 1⁄2. Affected participants may spread the taxes over a three-year period and may repay all or part of the distribution to the plan or any plan that accepts rollovers no later than the 3rd anniversary of the date of distribution. The allowable timeframe to take a CRD is January 1, 2020 through December 30, 2020.

A qualified individual may designate any eligible distribution as a CRD if the total amount that is designated does not exceed $100,000. It is important to note that a qualified individual may report the distribution as a CRD on their individual tax return even if the plan does not acknowledge the distribution as a CRD.

Coronavirus Loans – The CARES Act modified the rules pertaining to participant loans by allowing loans up to 100% of a qualified individual’s vested account, up to $100,000 (previouslylimited to 50% and $50,000, respectively). This provision covered loans issued from March 27, 2020 through September 23, 2020. In addition, loan payments due between March 27, 2020 and December 31, 2020 could be delayed up to one year and the five-year maximum loan repayment period was extended by one year.

The IRS recently clarified that only 2020 loan payments are delayed, and repayment, including accrued interest, must begin by the first loan payment due date in 2021. If payments were delayed, and a participant will take advantage of the extended repayment period, the loan must be reamortized from the first payment date in January 2021 to the end of the extended loan term.

Required Minimum Distribution (RMD) – The CARES Act allowed any participant with an RMD due in 2020 from a defined contribution plan to waive their RMD. This includes anyone who turned age 70 1⁄2 in 2019 and would have had to take the first RMD by April 1, 2020 and anyone who would normally take a delayed RMD by April 1, 2021. If an RMD was distributed prior to the enactment of the CARES Act, participants had the ability to roll over the RMD by August 31, 2020. The RMD waiver does not apply to defined benefit plans.

On Friday, June 19, 2020, the IRS released Notice 2020-50 which expanded the definition of a “qualified individual.” The following individuals are now considered qualified individuals:

- The individual, spouse, or dependent has been diagnosed with COVID-19 by an approved test;

- The individual suffered financially from the pandemic due to being laid off or furloughed, being quarantined, having work hours reduced, closing of a business owned by the individual, or being unable to work due to lack of childcare;

- Individuals having a reduction in pay due to COVID-19 or having a job offer rescinded or start date delayed due to COVID-19;

- The individual’s spouse or a member of the individual’s household being quarantined, being furloughed or laid off, having work hours reduced, being unable to work due to lack of childcare, having a reduction in pay, or having a job offer rescinded or start date delayed due to COVID-19; or

- Closing or reducing hours of a business owned or operated by the individual’s spouse or a member of the individual’s household due to COVID-19.

For purposes of applying these qualifications, a member of the individual’s household is someone who shares the individual’s principal residence.

Plan administrators can rely on the participant’s self-certification that they qualify for the distribution. The IRS provided a model self-certification that can be found here: irs.gov/pub/irs-drop/n-20-50.pdf.

THE SECURE ACT REMINDERS

WITH SO MUCH DISCUSSION SURROUNDING THE CARES ACT, IT IS EASY TO FORGET THAT 2019 BROUGHT US SOME OF THE MOST SIGNIFICANT CHANGES TO RETIREMENT PLAN LAW SINCE THE PASSAGE OF THE PENSION PROTECTION ACT OF 2006. This legislation came to us by virtue of The Setting Every Community Up for Retirement Enhancement (SECURE) Act that was signed into law on December 20, 2019. While many of the SECURE Act provisions are currently in effect, there are important provisions still to come that plan sponsors should be prepared for in 2021 and beyond. Highlights of the upcoming changes include:

Long-Term Part-Time Employees – Beginning with the 2024 plan year, long-term part-time employees who have attained age 21 and worked at least 500 hours per year for 3 consecutive years must be given the opportunity to make elective deferral contributions. While eligibility will not occur until the 2024 plan year, 2021 is the first year for which hours must be kept to determine if the 500 hours for 3 consecutive years requirement has been satisfied. It is important to note that these employees can be disregarded for non-discrimination testing purposes.

Pooled Employer Plans (PEP) – The SECURE Act established a new type of multiple employer plan (MEP) called a “pooled employer plan” (PEP). A PEP permits unrelated employers to come together to participate in one retirement plan that is administered by a “pooled plan provider” (typically a financial services company, recordkeeper, or third-party administrator). The SECURE Act allows pooled plan providers to start operating PEPs as early as January 1, 2021. Pooled plan providers must register with the Secretary of Labor and the Secretary of the Treasury prior to beginning operations.

Lifetime Income Disclosure – Under the SECURE Act, all defined contribution plans will be required to include a lifetime income illustration on annual participant benefit statements. The disclosure would illustrate the monthly payments the participant would receive if their total account balance were used to provide lifetime income streams. The DOL is expected to give more definitive direction to the format and content of the illustrations. Compliance is delayed until 12 months after additional guidance is provided by the DOL.